Learning about customers through the data collected through business and relationship management systems.

Presented by:

Larry Vincent, Professor of the Practice, Marketing

Presented to:

MKT 512

October 22, 2025

Behavioral data and customer profiling

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

Comparing options

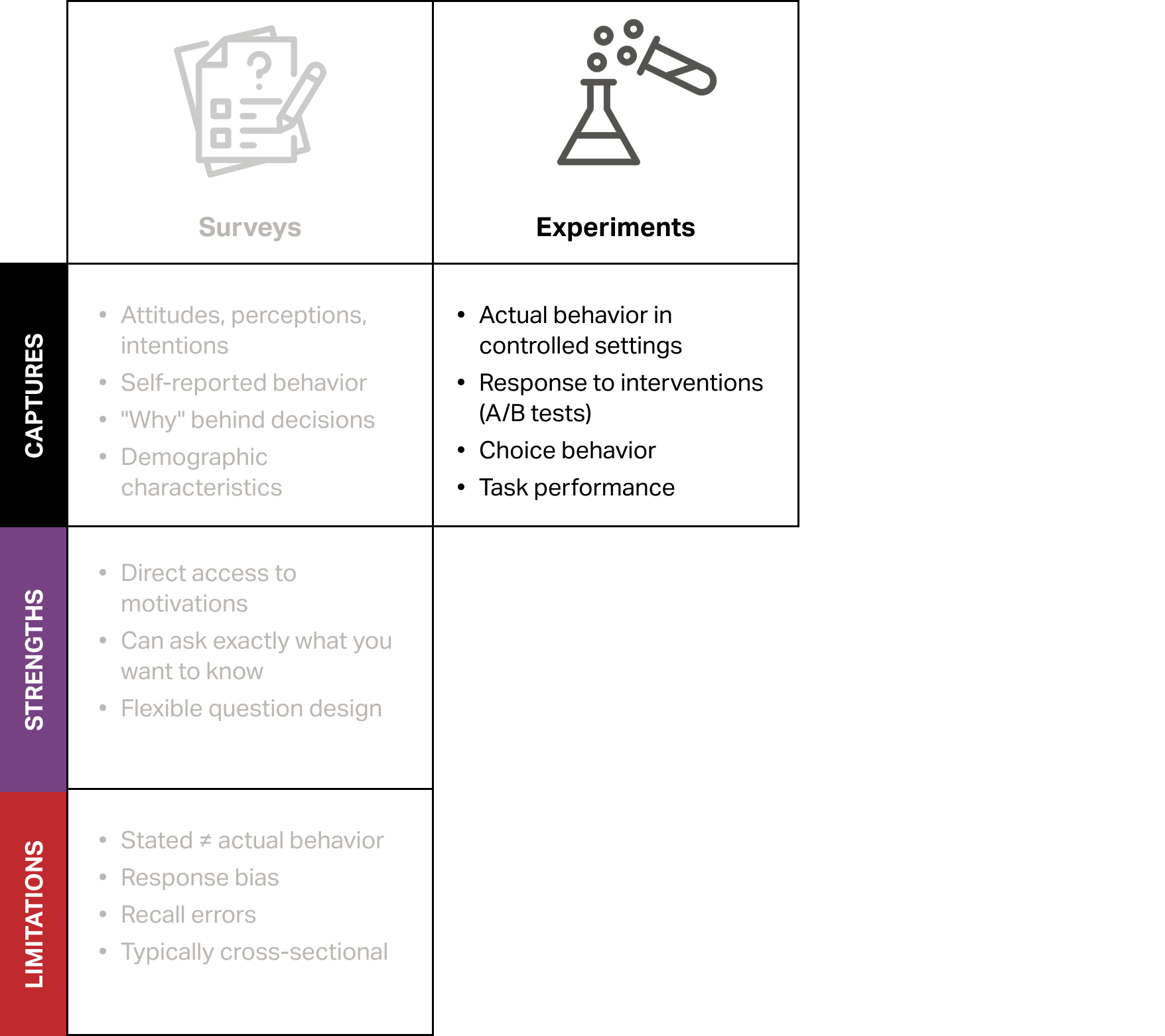

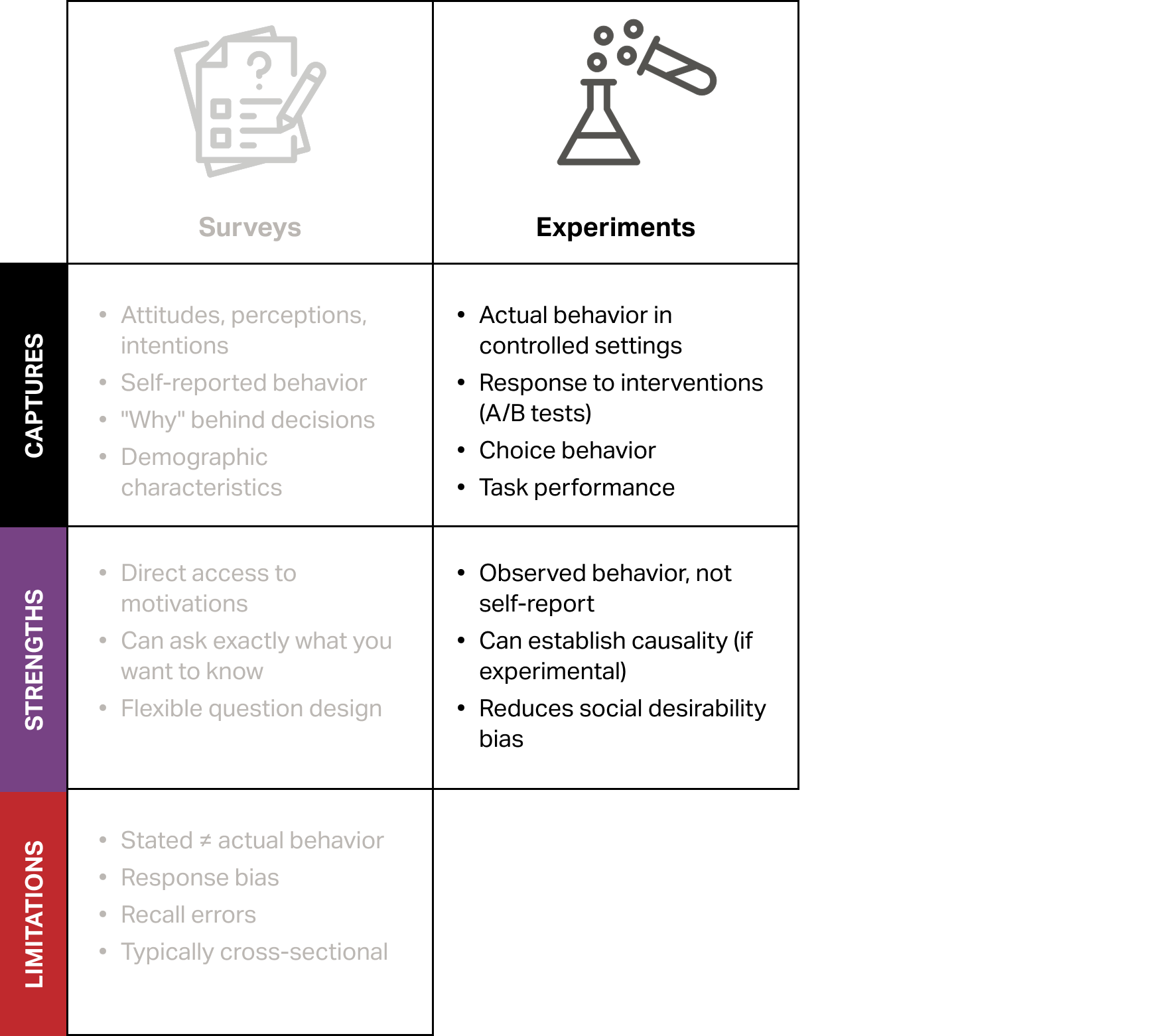

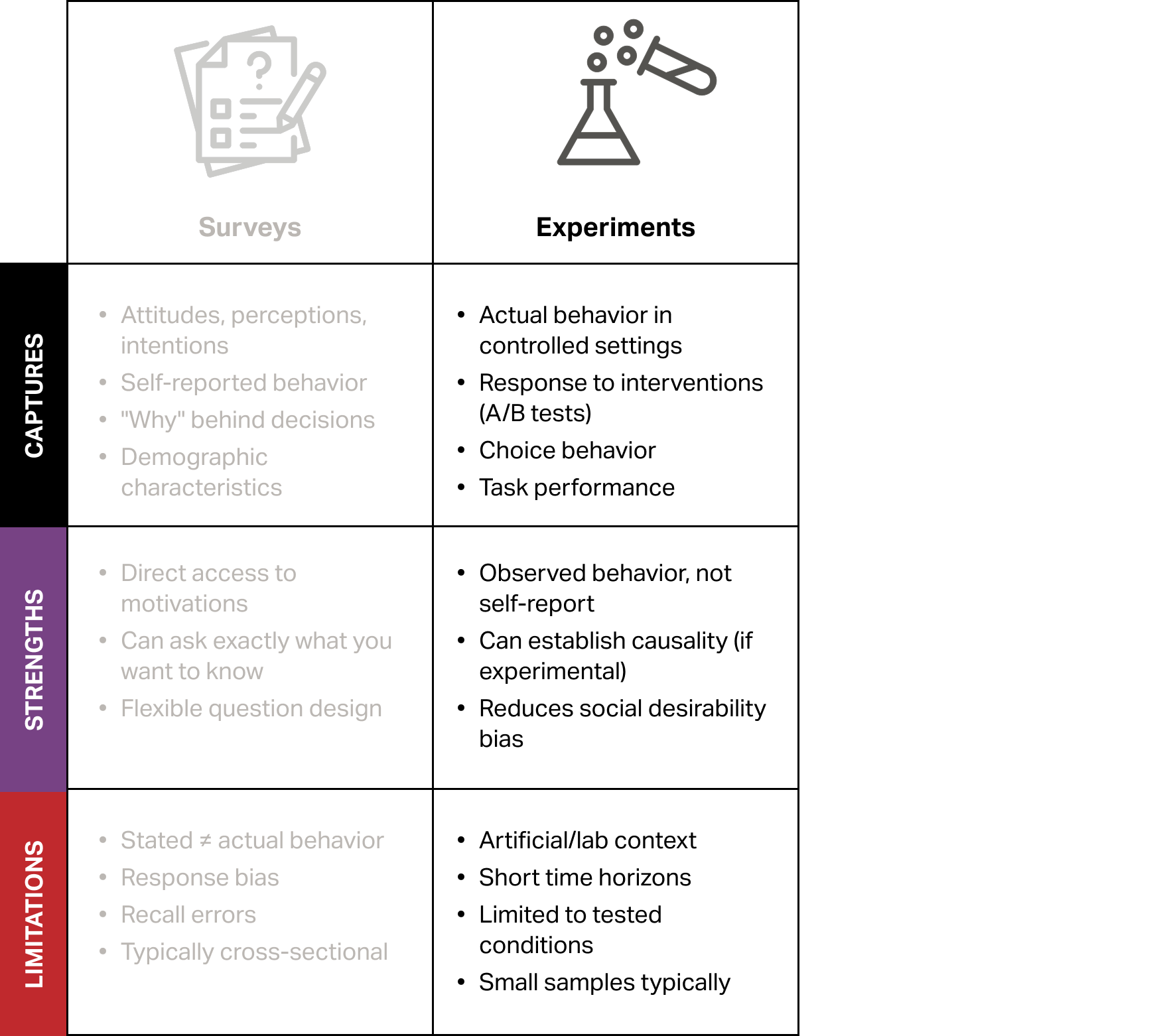

Stated preferences vs. revealed

Stated preferences vs. revealed

Most used behavior metrics

Recency–How recently have they engaged with us?

Most used behavior metrics

Recency–How recently have they engaged with us?

Frequency–How often do they tend to engage with us?

Most used behavior metrics

Recency–How recently have they engaged with us?

Frequency–How often do they tend to engage with us?

Velocity–Is their behavior accelerating, declining or stable?

Most used behavior metrics

Recency–How recently have they engaged with us?

Frequency–How often do they tend to engage with us?

Velocity–Is their behavior accelerating, declining or stable?

Monetary–How much do they typically spend or how much have they spent since originating?

Sample data

We will be working with a synthetic data set for a fictional company. The data set has four columns, transaction_id, customer_id, transaction_date, and transaction_amount.

File: customer-transactions-data.csv

transaction_id

customer_id

transaction_date

transaction_amount

TXN0000001

CUST04313

2023-01-01

118.43

TXN0000002

CUST00041

2023-01-02

111.25

TXN0000003

CUST00152

2023-01-02

118.83

TXN0000004

CUST00293

2023-01-02

54.96

TXN0000005

CUST00341

2023-01-02

139.38

TXN0000006

CUST00498

2023-01-02

83.58

Transforming to customer data

# Set a cutoff point--here it's the day after the last transaction dateANALYSIS_DATE <-as_date("2025-10-01")# Group by customer to calculate customer behaviorscustomers_df <- df |>group_by(customer_id) |>summarise(last_transaction =max(transaction_date),recency =as.numeric(ANALYSIS_DATE - last_transaction),frequency =n(),monetary =sum(transaction_amount),avg_tx =mean(transaction_amount) )

Transforming to customer data

# Set a cutoff point--here it's the day after the last transaction dateANALYSIS_DATE <-as_date("2025-10-01")# Group by customer to calculate customer behaviorscustomers_df <- df |>group_by(customer_id) |>summarise(last_transaction =max(transaction_date),recency =as.numeric(ANALYSIS_DATE - last_transaction),frequency =n(),monetary =sum(transaction_amount),avg_tx =mean(transaction_amount) )

The number of days (or time period) since a customer’s last transaction or interaction.

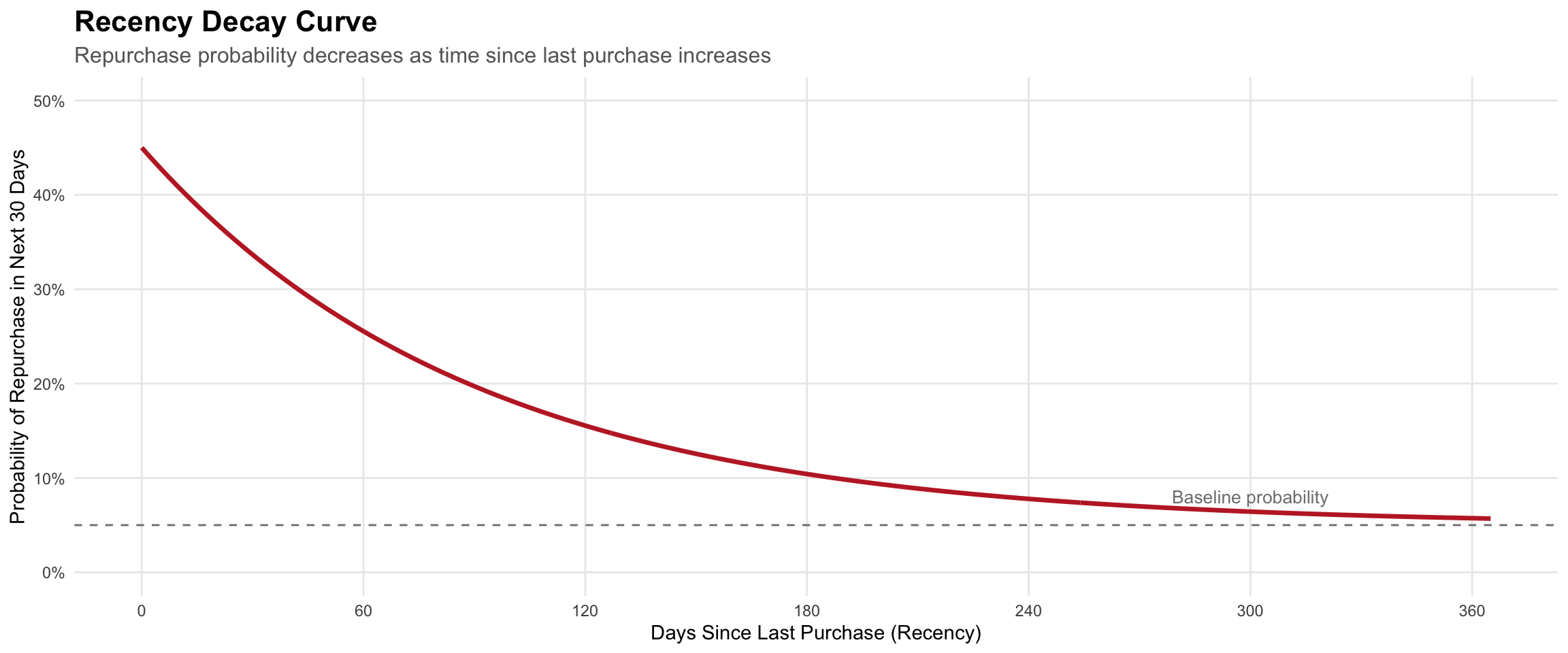

Decay curve

Customer repurchase probability decays over time, though the rate varies dramatically by category (fast-moving consumer goods decay quickly; durable goods like appliances show flat patterns).

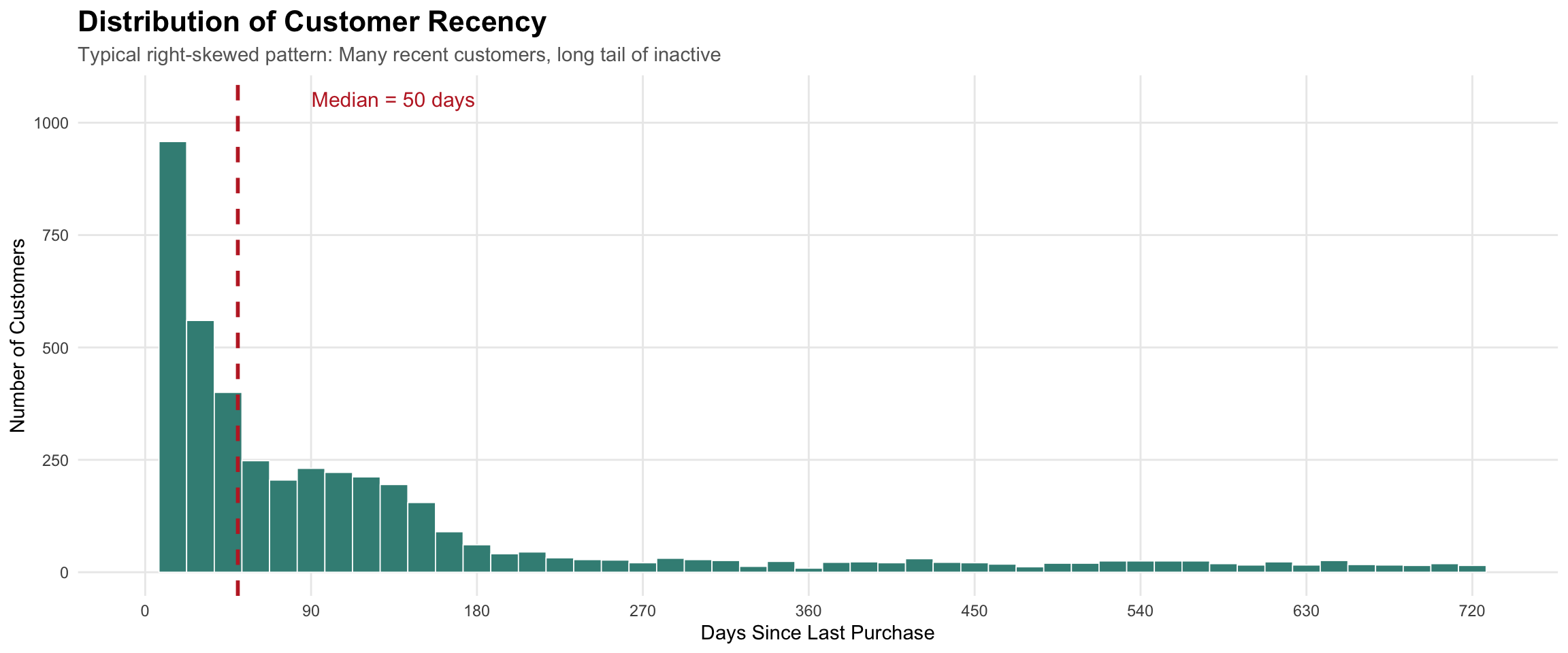

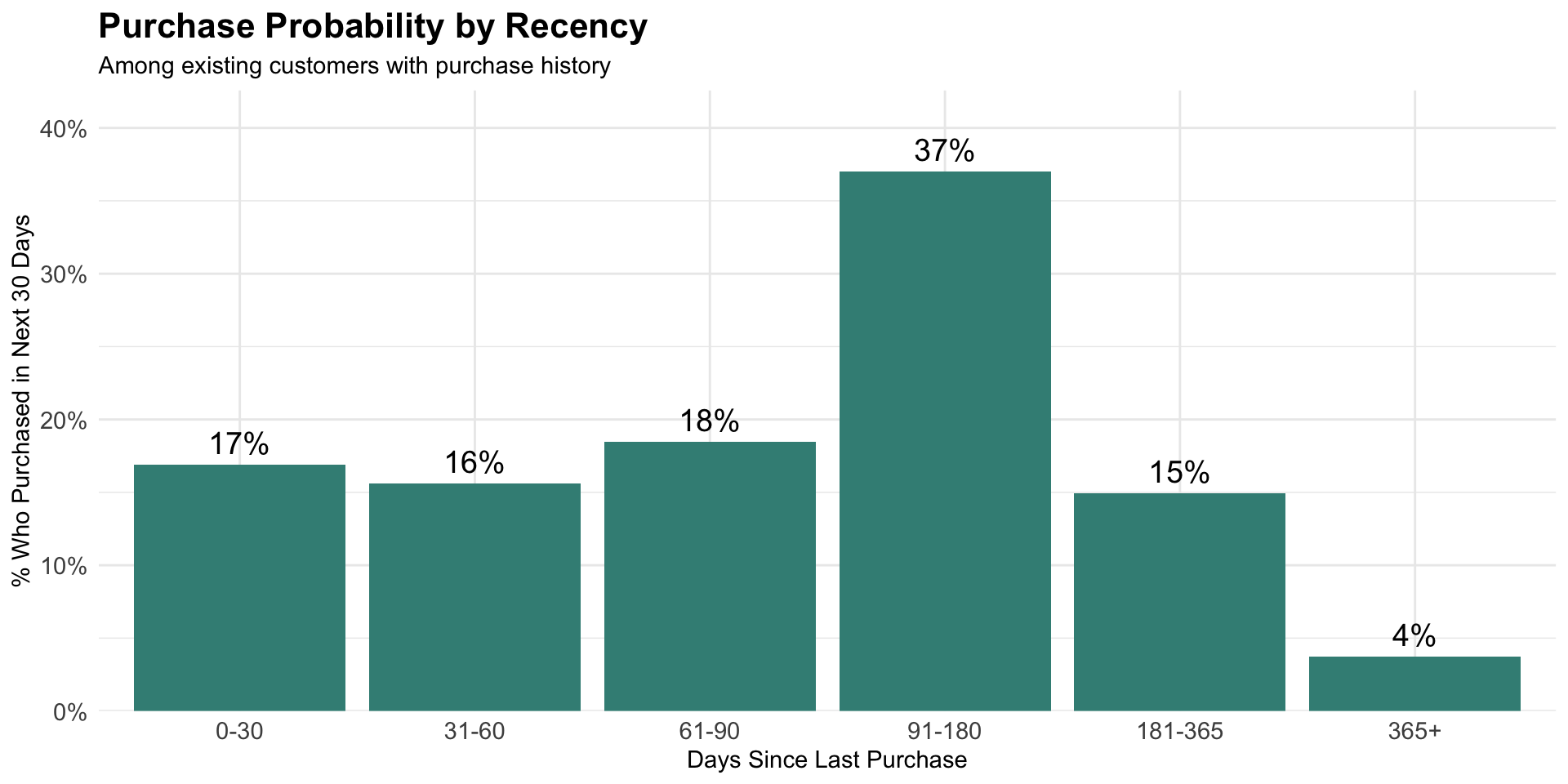

Analyzing recency patterns

Notice the concentration of customers with recent purchases (left side) and the long tail of inactive customers extending to the right—this pattern suggests most customers are engaged, but you have a significant inactive segment requiring re-engagement strategies.

Predictive Models

Recency scores can help us understand common patterns and probability of purchase within certain windows. These probabilities can be used to optimize marketing mix decisions.

Recency needs context

Two customers with same recency (30 days)

Customer A: Second purchase in < 30 days

→ Promising new customer

Customer B: Only purchase in 2 years

→ At-risk, declining customer

We need additional context

How often do they engage?

How much do they spend?

Are they accelerating or declining?

With this context, you can then develop strategy.

Winback lapsing and at-risk customers or take the win but don’t waste resources on inconsistent or opportunistic customers

Incentivize return visit from new customer or target for special offer/reward

Next: Frequency as the second behavioral dimension

Frequency

Frequency

The number of transactions or interactions a customer has made within a specified time period.

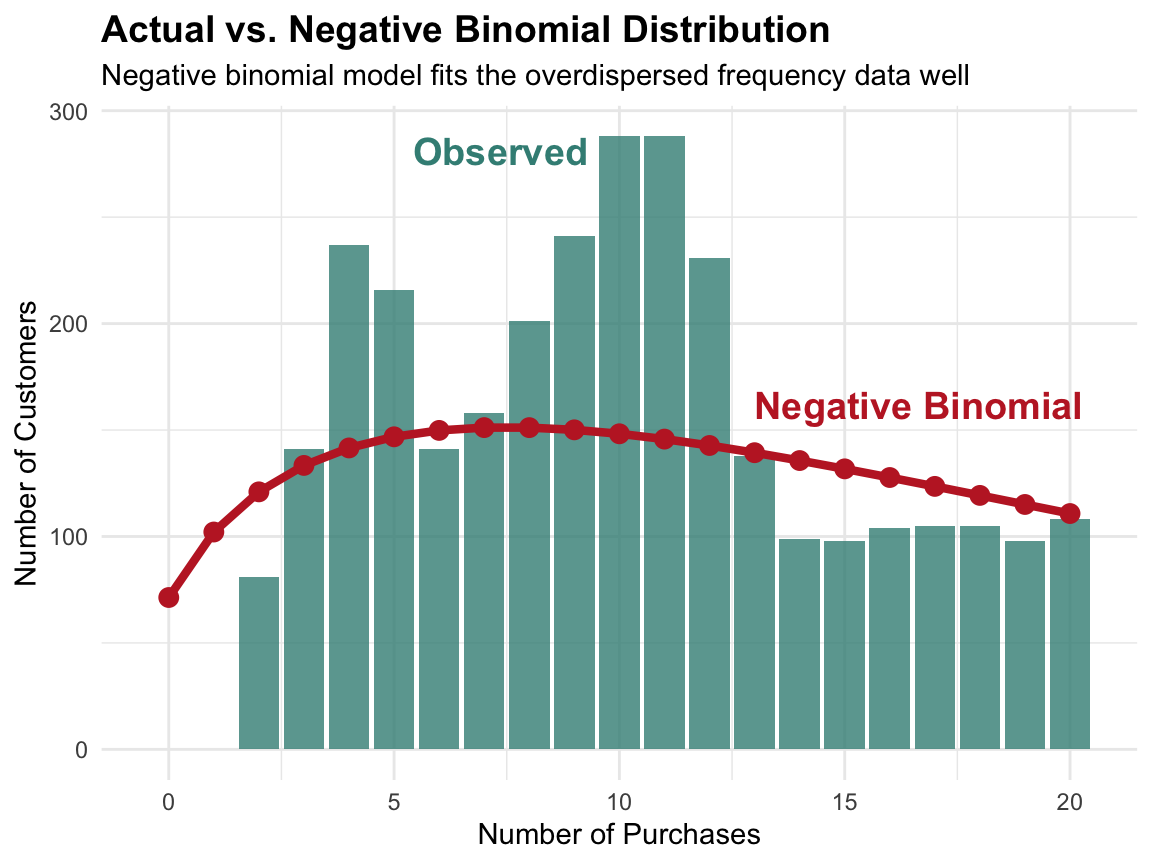

Frequency as count data

Frequency is count data (integers ≥ 0), which requires specialized statistical methods. When the variance exceeds the mean (overdispersion) or there’s excess zeros, negative binomial or zero-inflated models are more appropriate than standard linear regression.

Properties of Count Data:

Only non-negative integers (0, 1, 2, 3…)

Cannot be averaged meaningfully

Variance often increases with mean

Excess zeros common (many one-time purchasers)

Statistical approaches:

Poisson regression (if mean ≈ variance)

Negative binomial (if overdispersed)

Zero-inflated models (if excess zeros)

Frequency is context-dependent

What constitutes “high frequency” varies dramatically by business model and product category. A metric that signals engagement in one industry may indicate completely different behavior in another.

Business Model

High Frequency

Interpretation

Coffee Shop

20+ visits/month

Daily regular

Grocery Store

2-3 visits/week

Weekly shopper

E-commerce Fashion

8-12 orders/year

Fashion enthusiast

SaaS (B2B)

Daily logins

Power user

Luxury Auto

1 purchase/5 years

Repeat customer (rare!)

Streaming Service

Daily usage

Core subscriber

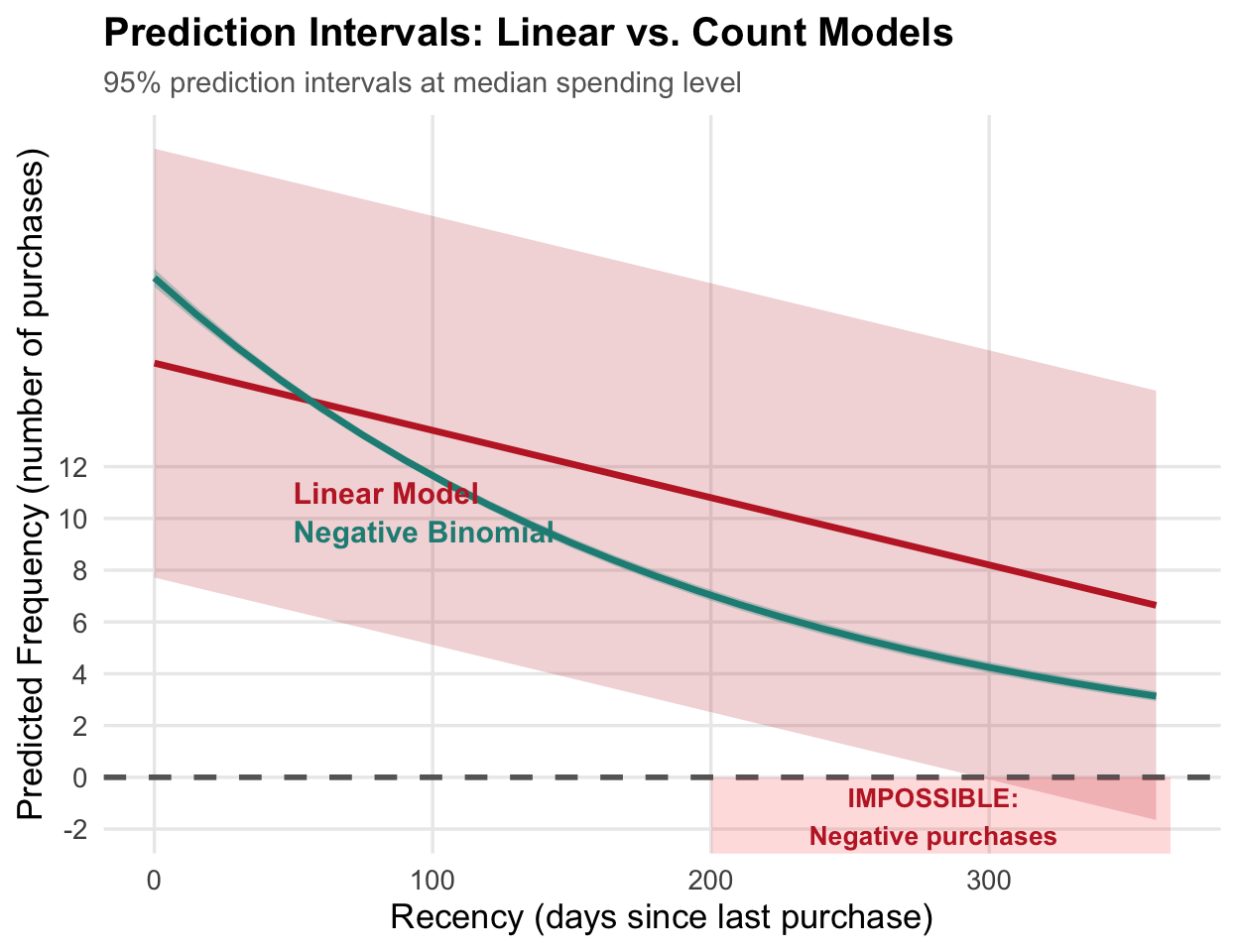

Count data requires care

Linear regression on count data produces nonsensical prediction intervals that include negative frequencies—an impossibility for count data.

# Wrong approach: Linear modellm_model <-lm(frequency ~ recency + monetary,data = customers_df)# Prediction intervalspredict(lm_model, interval ="prediction")# Right approach: Negative binomial# using glm.nb function from MASS packagenb_model <-glm.nb(frequency ~ recency + monetary,data = customers_df)

Key Problem: Linear model assumes constant variance and normal errors—both violated with count data.

Monetary value

Monetary value

The financial dimension of customer behavior, revealing spending patterns, preferences, and relationship depth beyond simple revenue totals

Beyond the total

Customer Profile

Lifetime Spend: $5,240

Transactions: 60

Time Period: 36 months

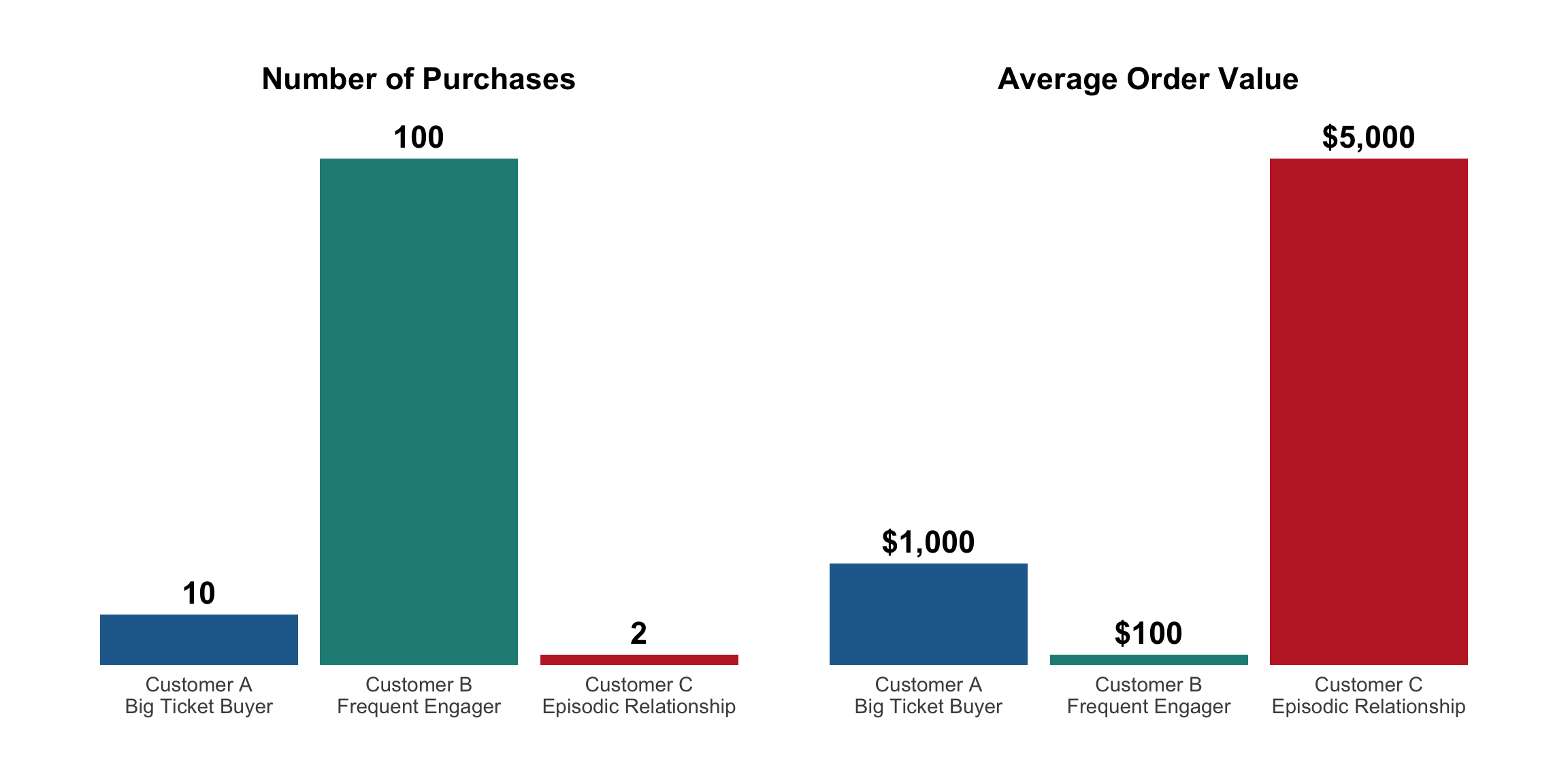

All revenue is not equal

Identical revenue ($10,000), completely different relationships and strategies needed

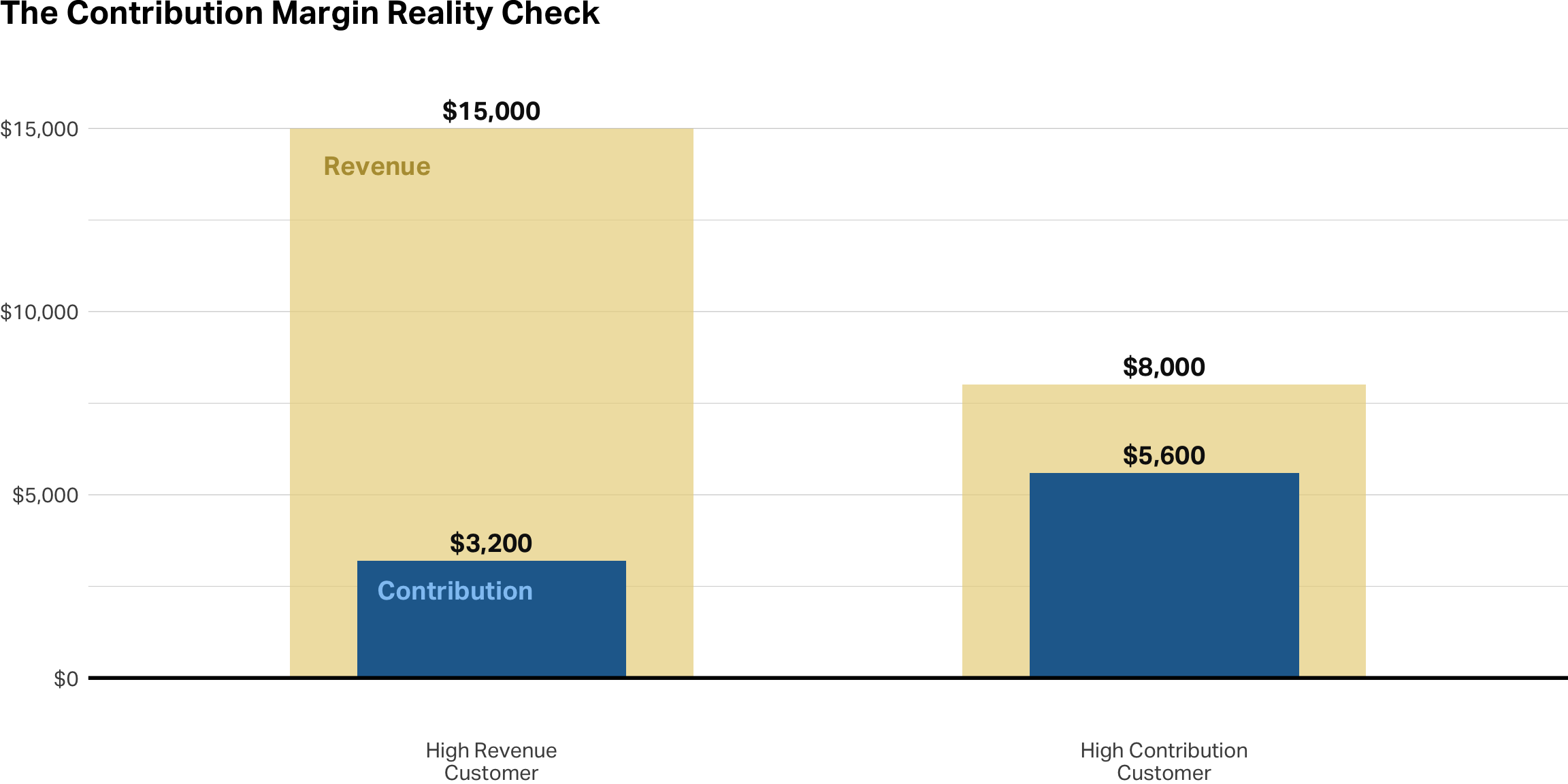

Revenue ≠ Value

Behavioral patterns (discount seeking, returns) directly impact true value

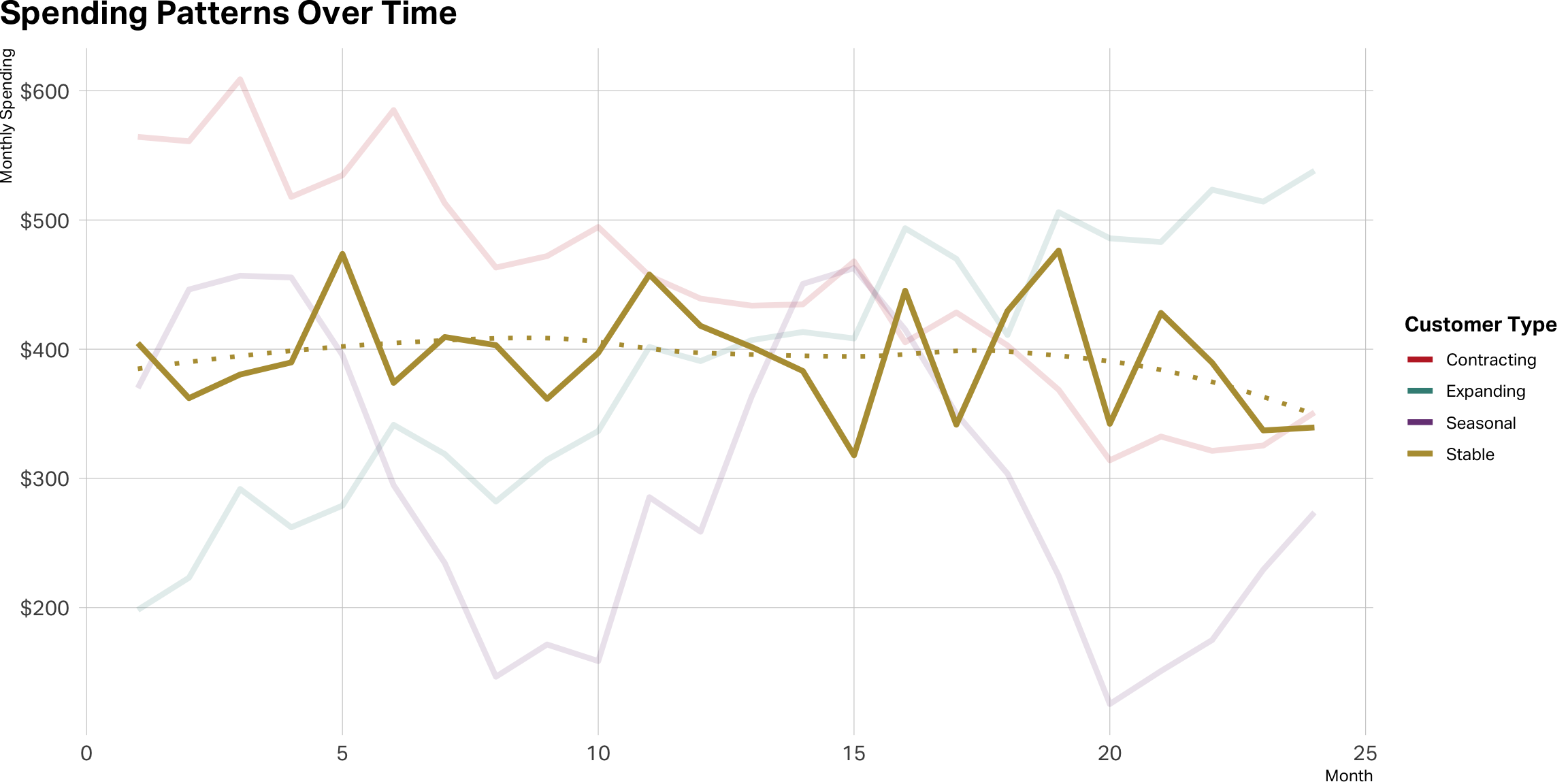

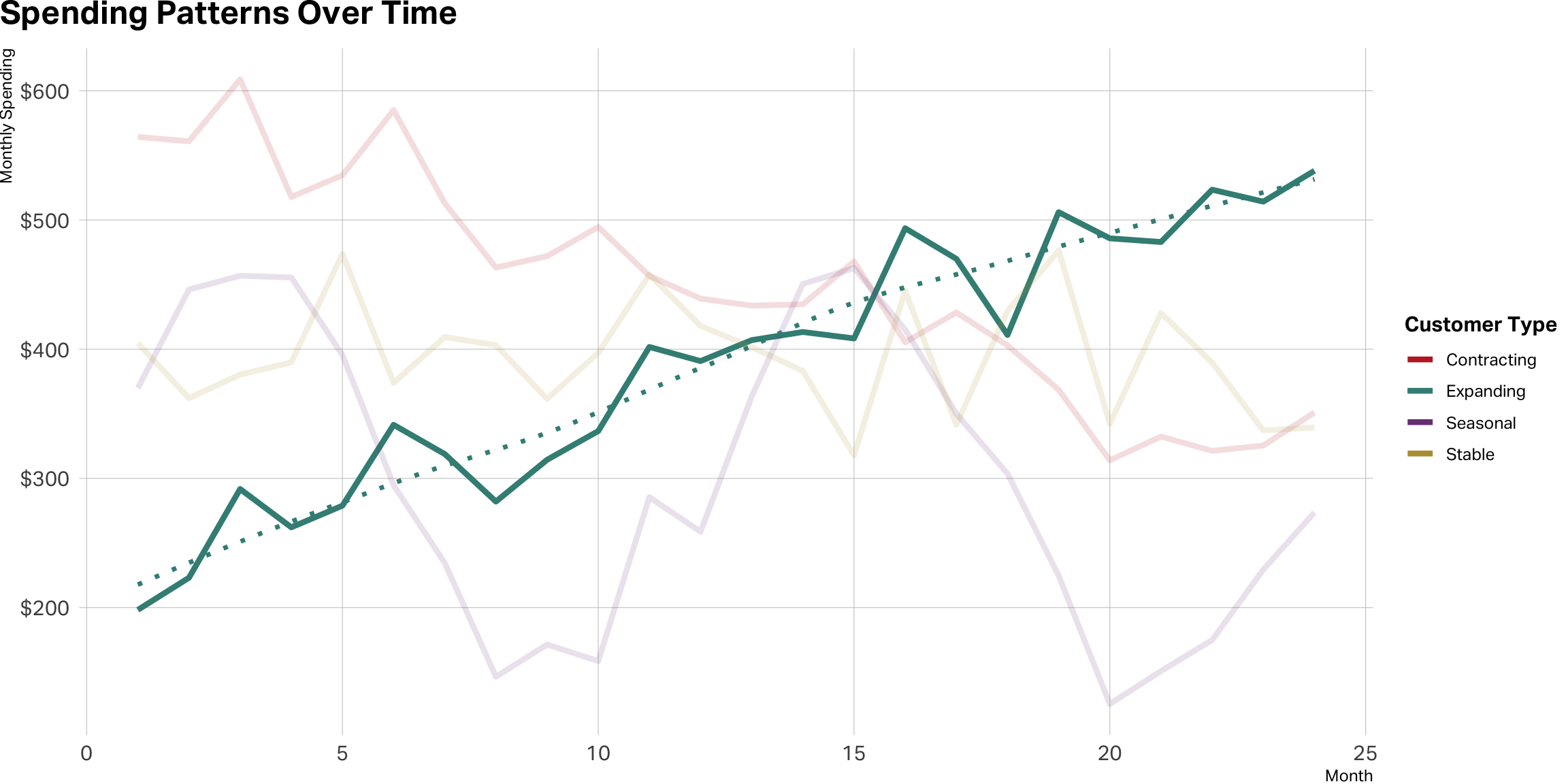

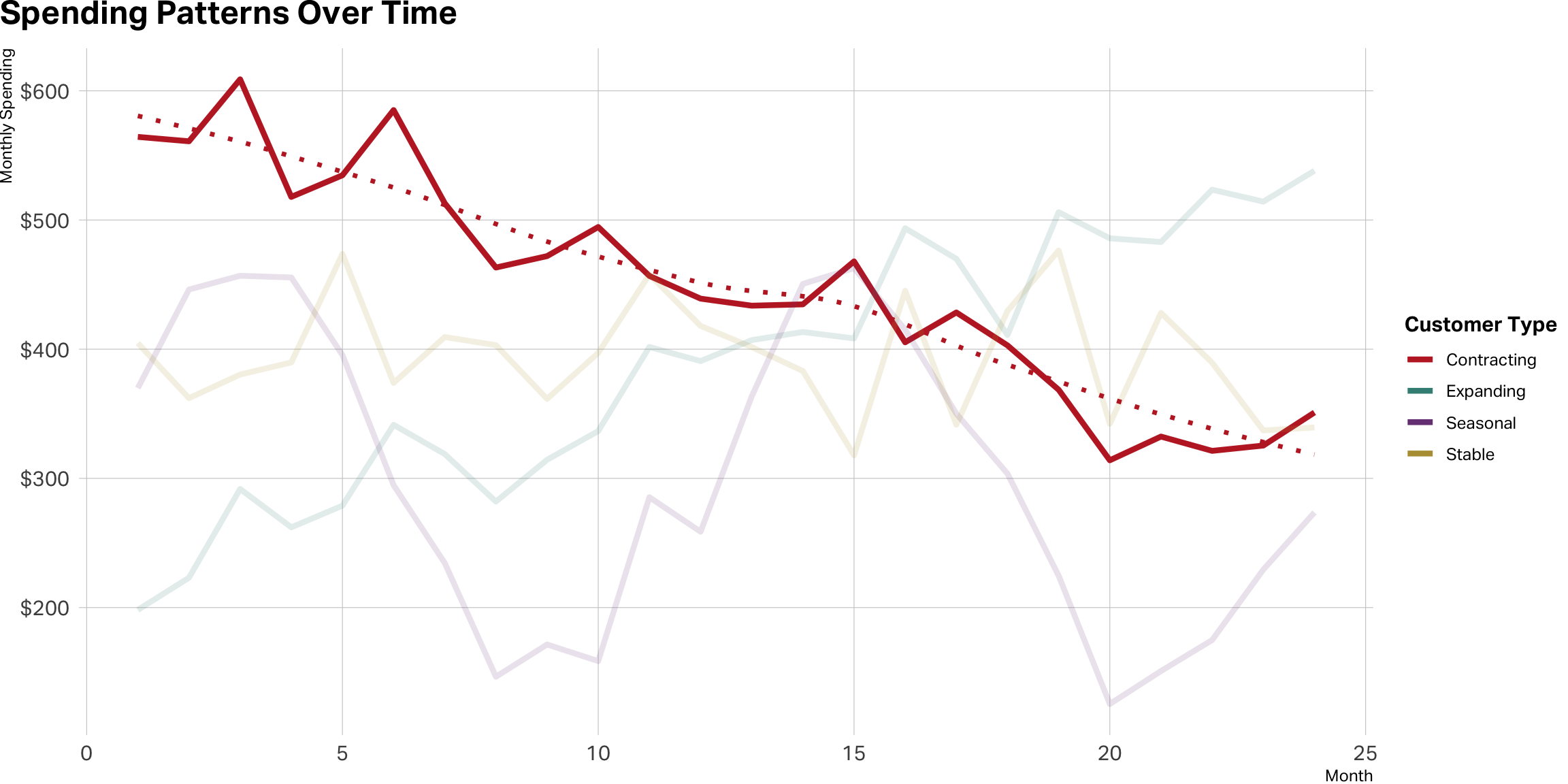

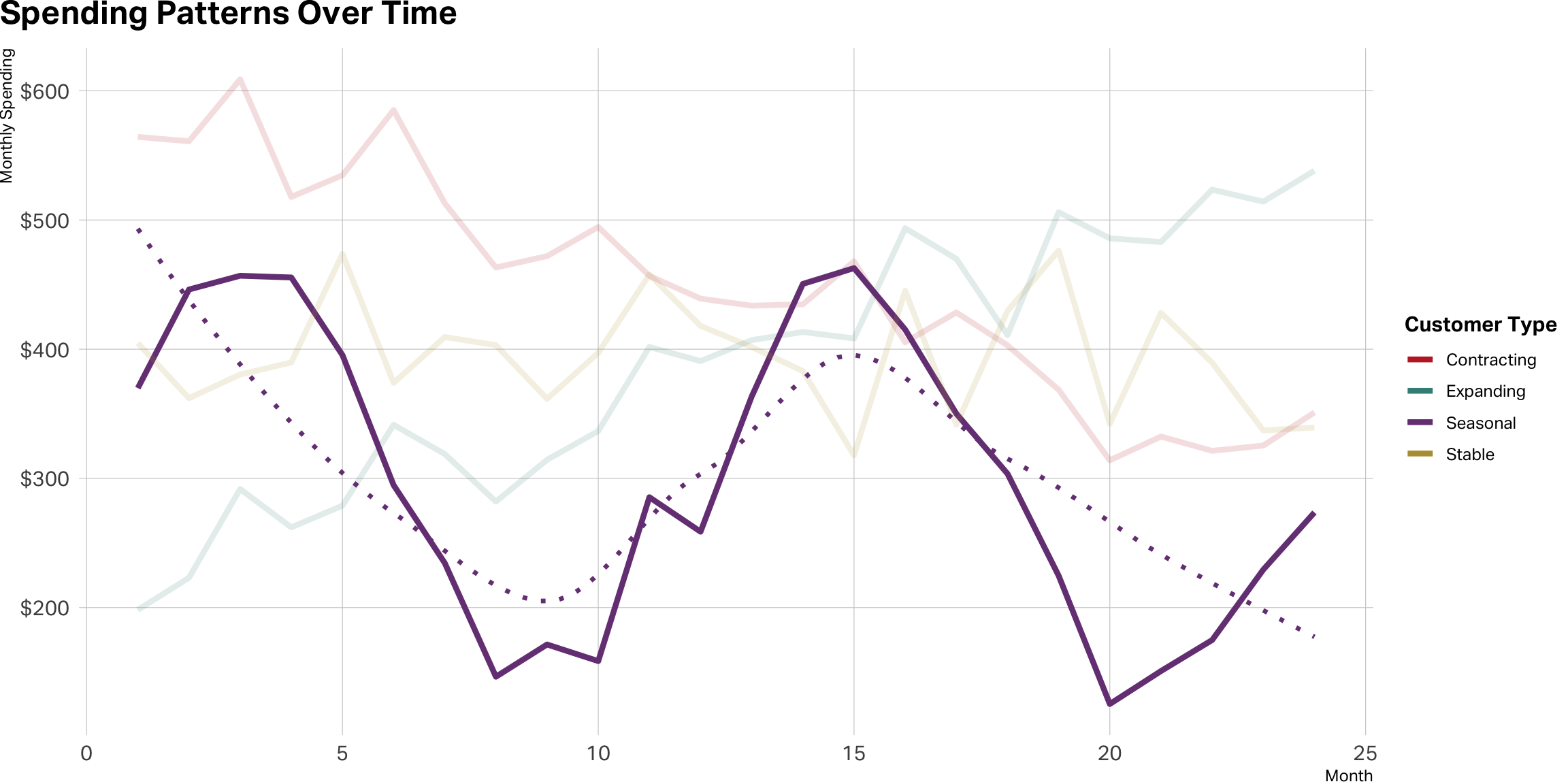

Stable is not a straight line

Lean in on expansion

Contraction is a red flag

Seasonal cases can be tricky

Takeaway

Monetary metrics are behavioral signals

Patterns reveal relationship depth, preferences, and trajectory

Understanding how customers spend is as important as how much

Next: Velocity — quantifying behavioral change over time

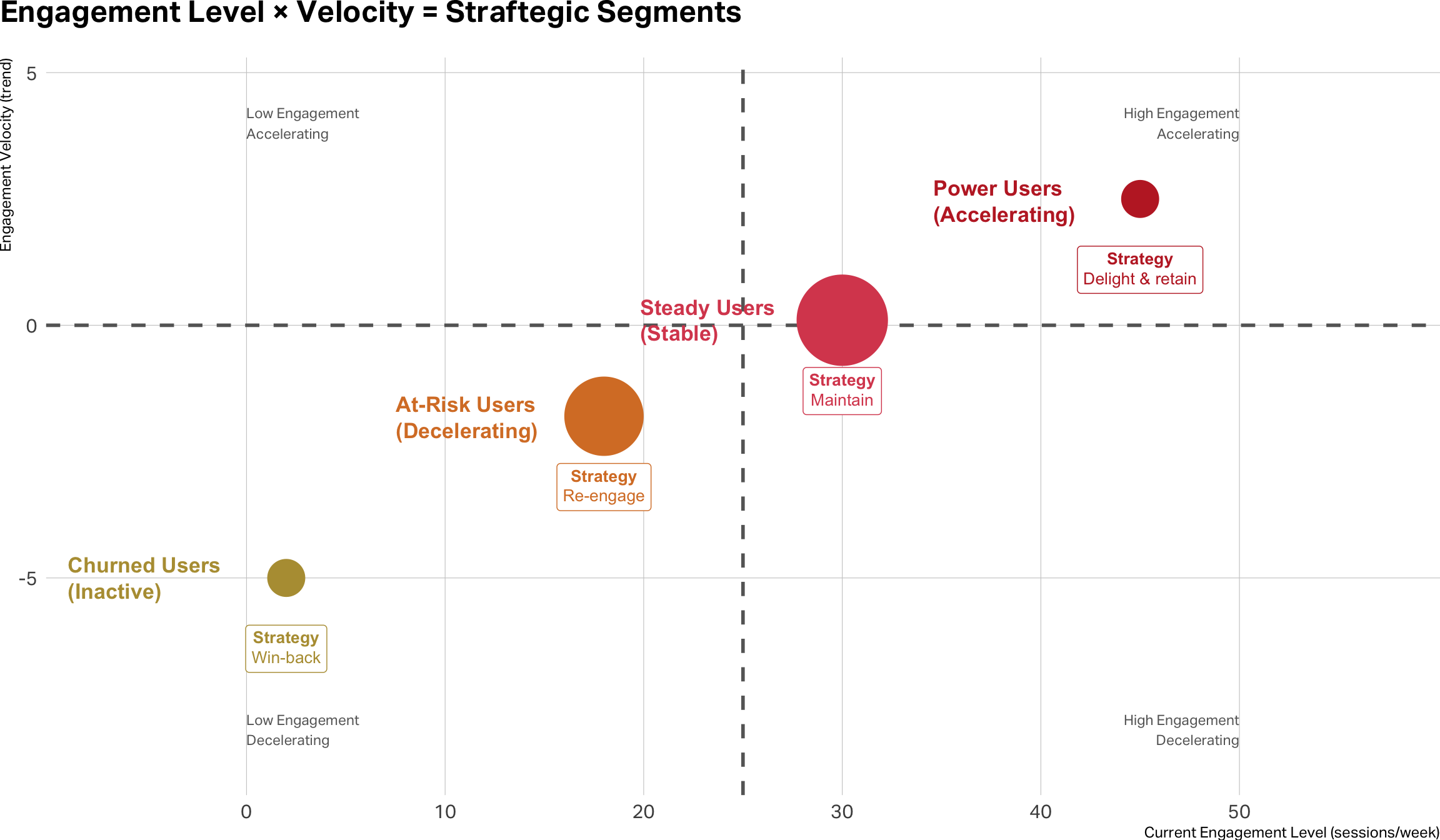

Velocity

Velocity

The rate of change in customer behavior over time, revealing whether engagement is accelerating, decelerating, or stable.

Velocity takes many forms

Context determines which velocity metric matters most for your business

Engagement Velocity

Login frequency trends

Content consumption patterns

Feature usage intensity

Session duration changes

Transaction Velocity

Purchase frequency changes

Time between orders

Repeat purchase acceleration

Spending Velocity

Average order value trends

Basket size growth

Wallet share expansion

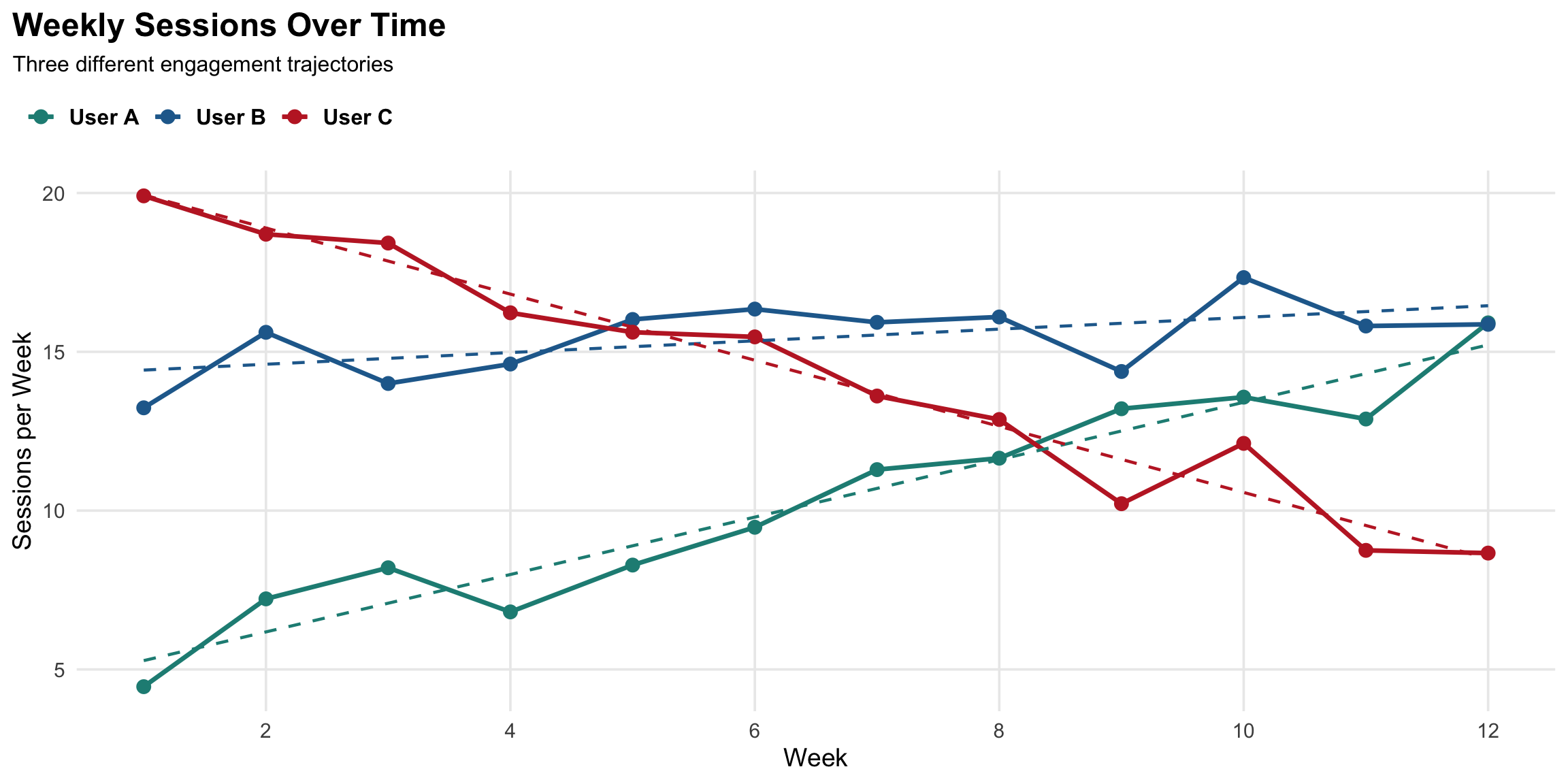

Measuring engagement velocity

Calculating velocity

Simple approach

Period-over-period change

Week 1-4 average: 8 sessions

Week 9-12 average: 14 sessions

Velocity = +75% growth

✓ Easy to calculate

✓ Intuitive to interpret

⚠️ Sensitive to outliers

Regression approach

Slope of trend line

model <-lm(sessions ~ week, data = user_data)velocity <-coef(model)["week"]# Positive = accelerating# Negative = decelerating

✓ Accounts for all data

✓ Less noise

✓ Statistical significance testing

Patterns vs. implications

Real-world velocity metrics

The specific metric varies, but the concept is universal: behavior change over time

Streaming (Netflix, Spotify)

Hours streamed per week

Content starts per session

Days active per month

Genre exploration rate

SaaS Products

Daily/weekly active users

Feature adoption rate

Time in application

Collaboration events

E-commerce

Days between purchases

Browse-to-buy conversion

Category expansion

Cart value trajectory

Social Platforms

Posts/comments per week

Connection growth rate

Engagement with content

Time on platform

Takeaway

Velocity adds the temporal dimension

Static metrics show where customers are → Velocity shows where they’re going

Early warning system for churn and expansion opportunities

Next: Bringing it together with RFM scoring

RFM Analysis

RFM Analysis

Combining recency, frequency, and monetary metrics to create actionable customer segments for strategic marketing decisions.

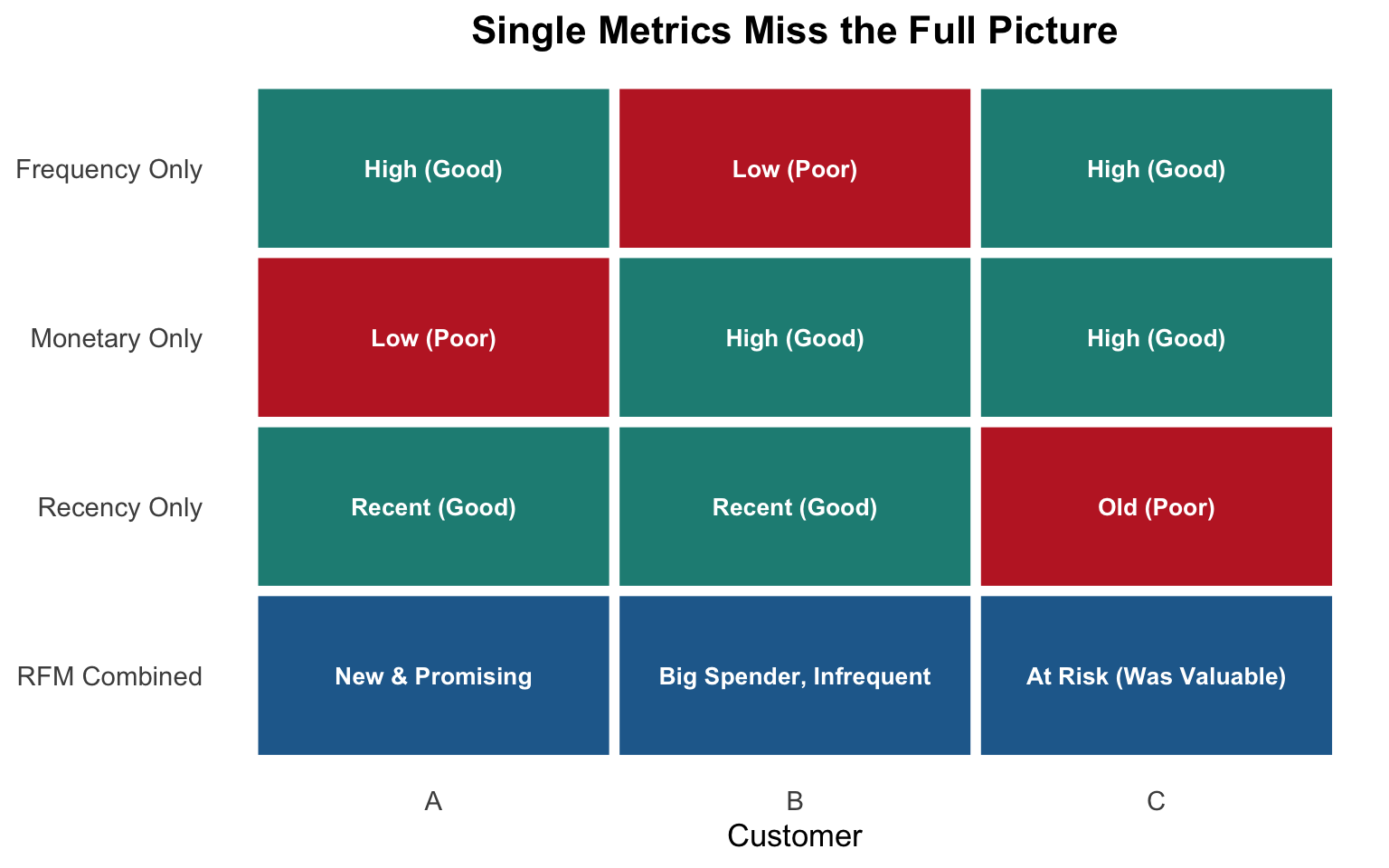

Why combine R, F, and M?

Each dimension alone provides incomplete information. Combined, they reveal distinct customer archetypes requiring different strategies.

Recency alone:

Can’t distinguish new customers from declining ones

Frequency alone:

Misses spending power and engagement timing

Monetary alone:

Ignores relationship trajectory and engagement patterns

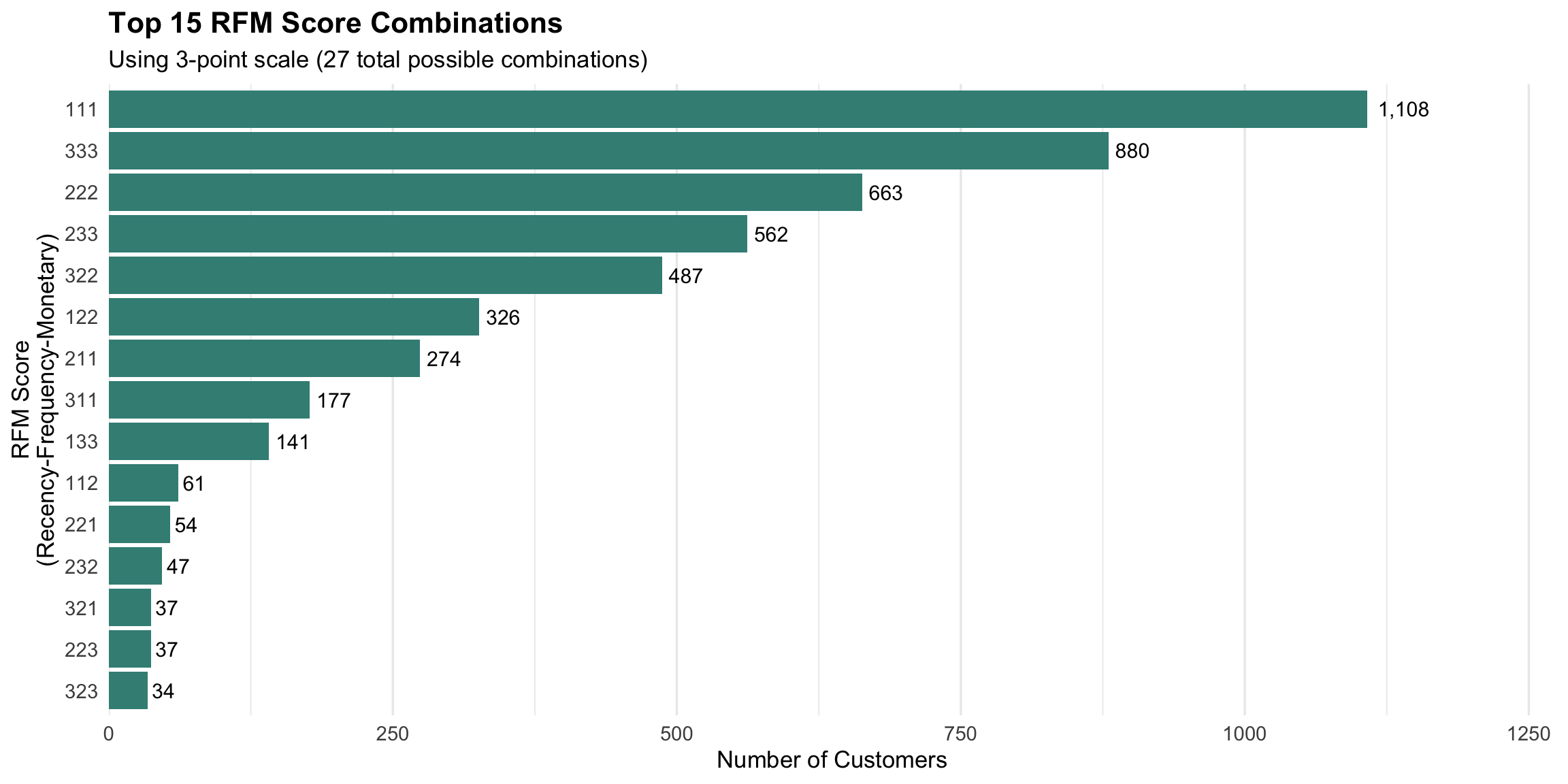

Creating RFM scores

Customers are ranked and divided into groups (typically 3-5) for each dimension, creating a composite score that enables segmentation.

Scoring Approaches:

Quintiles (5-point scale) - Divide customers into 5 equal groups - Score 5 = top 20%, Score 1 = bottom 20% - Creates 125 possible combinations (5³) - More granular, harder to interpret

Tertiles (3-point scale) - Divide customers into 3 equal groups

- Score 3 = top 33%, Score 1 = bottom 33% - Creates 27 possible combinations (3³) - Less precision, easier to act on

Understanding how customers distribute across RFM scores helps identify your most important segments and potential opportunities.

From scores to segments

Individual RFM scores are aggregated into business-relevant segments using rules-based logic, enabling targeted strategies for each customer group.

# Champions: High on all dimensionschampions <-filter(customers_rfm, R_score >=4& F_score >=4& M_score >=4)# Loyal: High F and M, decent Rloyal <-filter(customers_rfm, F_score >=4& M_score >=4& R_score >=2)# At-Risk: Were good (high F/M) but recency dropped at_risk <-filter(customers_rfm, F_score >=3& M_score >=3& R_score <=2)# Promising: Recent but unprovenpromising <-filter(customers_rfm, R_score >=4& F_score <=2)# Lost: Low on all dimensionslost <-filter(customers_rfm, R_score <=2& F_score <=2& M_score <=2)

Common RFM segments

Standard segment archetypes provide a starting framework, though specific definitions should be customized to your business context and customer lifecycle.

Segment

Typical RFM Pattern

Behavior Profile

Strategy Focus

Champions

555, 554, 544

Best customers: recent, frequent, high-value

Retention, VIP treatment, advocacy

Loyal Customers

X54, X55 (any R)

High value but may not be recent

Re-engagement, loyalty programs

Potential Loyalists

453, 354, 353

Recent, showing promise, building engagement

Accelerate frequency, increase basket

At Risk

255, 254, 155

Previously valuable, declining recency

Win-back campaigns, special offers

Need Attention

333, 233, 323

Moderate on all dimensions, unclear trajectory

Targeted nudges, prevent decline

Promising

511, 411, 311

Recent first-time or low-frequency buyers

Onboarding, second purchase incentive

Hibernating

244, 155, 154

Long inactive but had some historical value

Aggressive win-back or deprioritize

Lost

111, 112, 121

Unlikely to return, minimal engagement

Win-back with cost constraints or ignore

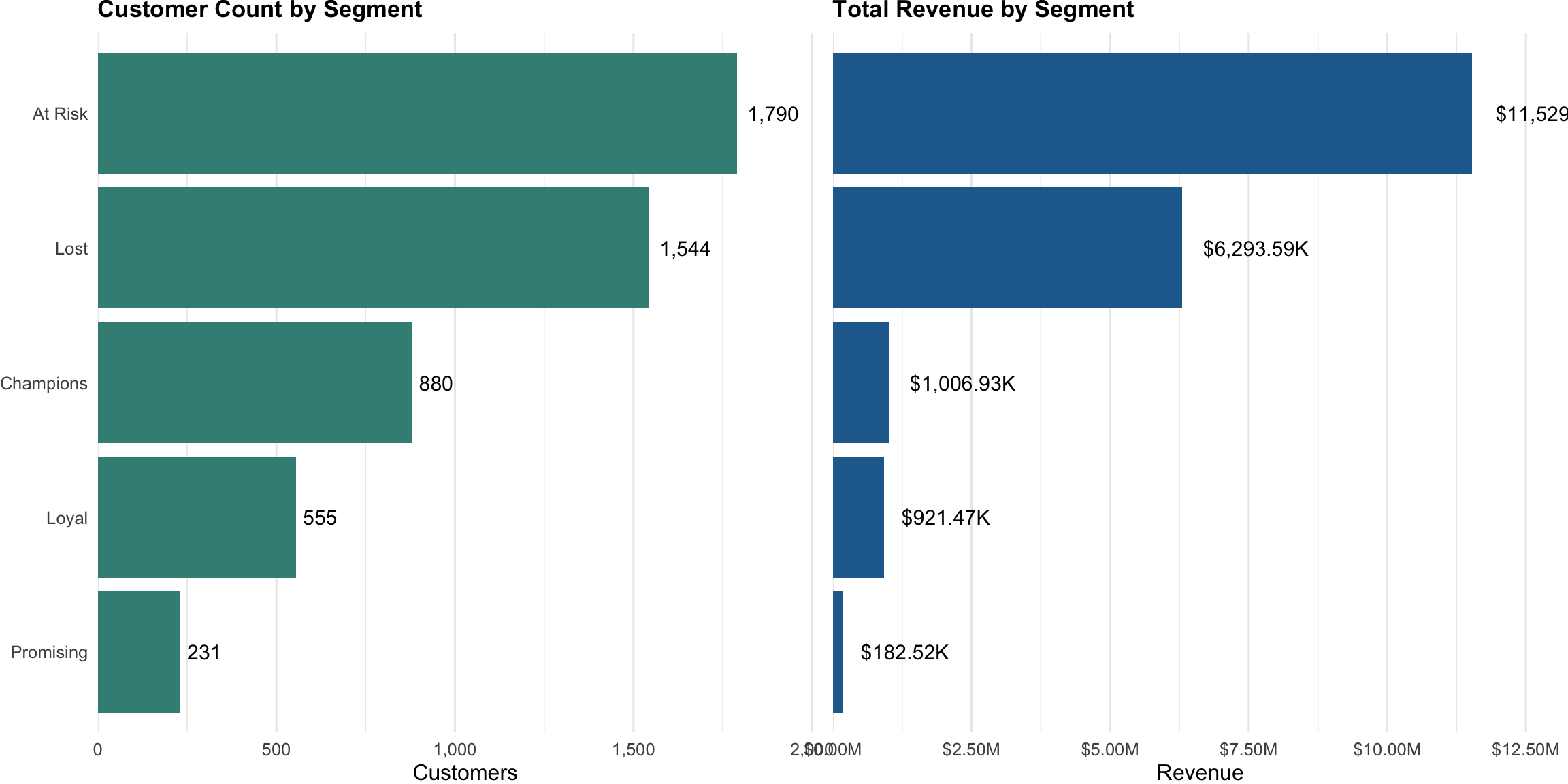

Segment profile analysis

Profiling segments by size, revenue contribution, and average metrics validates segmentation logic and informs resource allocation decisions.

RFM limitations

While powerful for segmentation, RFM has constraints that more sophisticated clustering techniques can address in advanced analysis.

What RFM Does Well

Simple, interpretable framework

Actionable segments with clear logic

Works with minimal data requirements

Business stakeholders understand it

Computationally efficient

Good baseline for many businesses

What RFM Misses

Arbitrarily groups continuous variables

Loses information in discretization

Can’t capture complex, non-linear patterns

Fixed rules may not fit all customers

Ignores product/category preferences

No statistical validation of segments

Misses velocity and trajectory nuances

Takeaway

RFM transforms individual metrics into strategic segments

Provides actionable framework for differentiated marketing

Foundation for understanding customer value and lifecycle

Starting point for more sophisticated analytical approaches